As the industry is facing tough competition, every area needs to be strengthened for survival. Rejection control is one of the key areas where cost can be controlled and profitability can be increased. Nowadays, companies practice zero per cent rejection in formal garments where fabrics are of good quality. Under zero percent methodology, defective cut parts during manufacturing get replaced with new cut parts. But is it zero per cent in real term? The answer is ‘No’ as there are rejections of cut parts and fabric cost involved is not actually taken into calculation. The fabric getting used for defective part replacement is cost to the company. Normally rejections are considered from cutting aspect but factory cost is involved right from fabric utilisation. Therefore rejections are never truly zero per cent and companies must develop mechanisms to get it controlled within the permissible limit. The ideas to control rejection are discussed below:

Develop permanent guideline criteria: Based on the type of business, companies need to develop guidelines which will be applicable to any style going to be manufactured. It is only an idea and may differ from company to company based on the product line and historical experience.

Pre-production technical (R&D +IE) department function:

Pre-production technical (R&D +IE) department function:

At the time of sampling and order finalisation, the pre-production technical (R&D +IE) department evaluates every style according to the above guideline. After evaluation, they provide pre-budget for every style going to be manufactured. The budget information then goes to the production team through style file.

Fabric to cutting monitoring:

As cost is involved, the rejection should be considered right from the fabric. When we consider it from cutting aspect, the gap between fabrics and cutting gets shaded.

For example,

Style X has 1000 units order quantity

The marker average is 2 metre per garment

Fabric received from mill is 2200 metre

The order may go 5% plus which means shipping around 1050 pieces

As per the rejection guideline, this belongs to 1.5% rejection

Cutting plan quantity: 1000 +5% +1.5% = 1066 pieces

Actual cutting: 1060 pieces

Actual shipping: 1045 pieces

Rejection: @ from fabric 5%; @ from cutting 2%

In analysis, we may see below:

Fabric available was for 1100 pieces; actual cutting was for 1060 pieces

Actual realisation less than material available = 40 pieces

This 40 pieces less realisation may be because of many reasons such as

a) Defective fabric getting excluded while bulk cutting. Sometimes, fashion fabric gets damaged at one side of the fabric roll or in between the length. It gets passed in 4-point inspection method but while cutting, many new methods need to be implemented which are as follows:

- cut with side wastage of fabric;

- 2. cut in single piece lay to avoid defects in fabric;

- cut with frequent fabric tear and bad part out from layer;

- cut with different fabric or paper identification on top of the bad part in layers and later replacing that part by part change

- cut and 100% part checking to replace bad parts etc.

In all the above such cases, before bulk cutting, the information must be shared with fabric mills to bear the cost of rejections so that factory rejection gets minimised.

b) Fabric L short: Fabric is folded in 97 cm instead of 100 cm mark

c) Fabric beyond limit shrinkages during mass manufacturing

d) Fabric quantity written on top of the roll may be less in actual. May get this information from the cutting layer report, where every individual fabric roll entered and their realisation is noted

e) Mismanagement of fabric by cutting in bulk (info from layer report)

f) In bulk cutting, the end parts are more than the plan taken (info from layer report)

To know the correct reason and for future control, daily fabric reconciliation report needs to be made which would include how many units were supposed to be cut in one particular style but in actual how many cuts were made and the reason behind the balance not cut. In bigger order quantity, after 20% cutting, the fabric realisation must be checked in bulk cutting. This may be considered as fabric reconciliation and actual production average.

Sewing area monitoring: This includes the number of garments that have undergone cutting and have been loaded to sewing lines, so that the final output tallies with the loaded cutting. The rejection controller must tally the daily production report. Any style that is over from sewing must close all repairs and rejections.

Sewing area monitoring: This includes the number of garments that have undergone cutting and have been loaded to sewing lines, so that the final output tallies with the loaded cutting. The rejection controller must tally the daily production report. Any style that is over from sewing must close all repairs and rejections.

Through daily quality reports, the supervisor must find the information of rejection generating area and find control on the root itself. Daily repairs are key to keeping sewing area rejection within control. Rejection controller visits and tallies cut parts to find out any unattended repairs. If he finds any, then he submits it in the daily rejection report (shared below) for the manager to take action.

Finishing / packing monitoring: Finishing output must tally with the total number of garments received from sewing. Also defective pieces should be sent back to sewing with record for repair on daily basis as this is the key to keep rejection in control. It has been seen that packing gets finalised even without knowing the actual cut and make quantity. In that case, garments unknowingly get leftovers in production area. These garments keep floating into production after the shipment is moved out from the factory.

The simple and most important thing is to put the barrier into packing list quantity finalisation as it should be based on cut and make quantity. One simple and quick format for ready garment reconciliation before final packing list is made will help to control this process. This ensures that no good pieces are left behind after the shipment of the ex-factory. Example is as given below:

Rejection monitoring cell function

Rejection monitoring cell function

If we calculate rejection in monetary terms, it is a huge amount. For example, if one company is doing Rs. 700 average value product and monthly it is producing 2,00,000 garments with 3 per cent rejection rate. In value terms, it will be 6000 units X Rs.700 = Rs. 4,20,0000 (total rejection value). If it is able to reduce rejection rate by 1 per cent, it will be Rs. 1,400,000 increase in profitability or decrease in cost. Yearly, the total rejections will be Rs. 5, 04, 00,000 and when rejection rate is reduced to 1 per cent from 3 per cent, then Rs. 1, 68, 00,000 will be saved.

Therefore, allocating one employee to monitor and control rejection is a wise decision. One employee may be able to monitor and control till 500 machines output rejection. More than that quantity will require more number of employees to get involved in. This will depend on the type of business too.

The rejection controller’s job will be:

- have information on complete plan of manufacturing

- fabric reconciliation follow-up during production

- during production, following up for every area rejection such as cutting, embroidery, handwork, sewing, finishing etc.

- For having full control, using rejection guideline as parameter (shared in beginning), filling fabric reconciliation report (shared in fabric discussion), filling rejection control chart as shared below and mandatorily filling complete ready leftover pieces analysis report (shared in finishing / packing discussion) before finalising the packing list

Below is the rejection controller’s daily rejection report for managers to control on daily basis. This report provides information on the daily rejection and repair status of every department:

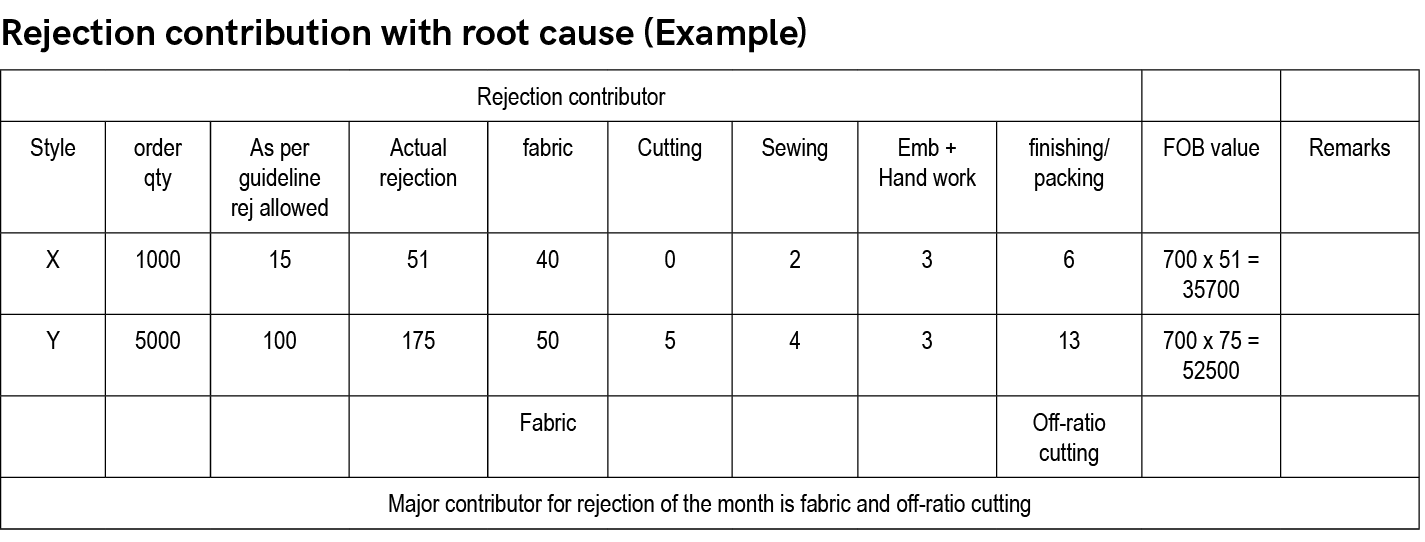

At the end of the month, rejection discussion in MIS:

At the end of the month, rejection discussion in MIS:

As stated earlier, rejection is huge money for any organisation. In final analysis chart, managers may see the key area from where more rejection is happening on a daily basis and the same will be controlled by working further on the problematic area. Rejection must be analysed and discussed by the managers to keep the organisation healthy.

Remember, if we reject bad quality at the time of: (a) fabric, it is 0% cost to the company as the cost will go to the supplier; (b) if we reject at the time of cutting, then fabric + cutting cost; (c) if we reject after sewing, then fabric+ cutting + sewing cost and if we reject in finishing / packing, then entire cost is lost. Therefore rejection stopped at the early stage is lesser cost to the company.

1 guideline chart, 3 reporting formats and 1 MIS chart analysis are the main tools of the rejection controller. As the amount involved is crores of rupees, it is highly recommended to adopt this process of monitoring and control. It will keep the organisation healthy and fit for survival. All the above may be taken as an idea. The type of product one organisation does or based on the strength and weaknesses of the organisation, the criteria and control methodology of rejection may change.